Allowance For Doubtful Debts / Chapter 8 Reporting and Interpreting Receivables, Bad Debt ... - It is an unavoidable cost of doing.. The allowance for doubtful debts is created by forming a credit balance which is netted off against the total receivables appearing in the balance sheet. Doubtful debt is money you predict will turn into bad debt, but there's still a chance you will receive the money. The statement contains the following information The allowance, sometimes called a bad debt reserve, represents management's estimate of the amount of accounts receivable that will not be paid by. Accounting for doubtful debts presupposes credit sales, so begin by recording the sale in the general journal.

Bad debt expense is the loss from doing business with customers who are later unable to pay for the services or goods they received. The bad debt expense for the accounting period is recorded with the following percentage of accounts receivable method journal. Bad debt expense is the uncollectable account receivable when the customer is no longer able to pay their outstanding debt due to financial difficulties or even accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. This method allows us to make an estimate, throughout the year, while our revenue is being recognized and our a/r balances are accumulating. Allowance for doubtful debts or also known as provision for doubtful debts are liabilities that we allocate for any possible non payment by the debtors.

Calculation and entries of bad debts Expense and Allowance ... from i.ytimg.com By writing off the debt through allowance for doubtful accounts, outstanding accounts receivable will be reduced. Allowance for doubtful accounts, bad debt expense accountanting steps when customers who owe do not pay. This method allows us to make an estimate, throughout the year, while our revenue is being recognized and our a/r balances are accumulating. This is usually expressed as a % of closing trade receivables and is usually estimated on the basis of past trend and future expectation about the. The allowance for doubtful accounts is a contra account that records the percentage of receivables expected to be uncollectible. How business firms face the reality that not all of their customers are going to pay what they owe. The statement contains the following information Unlike bad debt, doubtful debt isn't officially uncollectible debt.

We can make these estimates even if we do not yet know which accounts will not be.

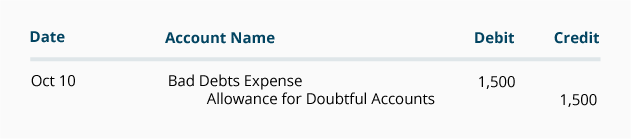

The expense is booked to the general ledger once all credit and collection efforts on a client's account are utilized and exhausted. The statement contains the following information It is an unavoidable cost of doing. This works in the same way as accumulated depreciation is deducted from the fixed asset cost account. Although sometimes, it may be an exact figure, as we'll see below. Bad debt expense is the loss from doing business with customers who are later unable to pay for the services or goods they received. The percentage of sales method and the accounts. Allowance for doubtful debt, on the other hand, gives an accurate matching of the financial records as it adheres to the matching principle. So it is kept on the liabilities side of the balance sheet. The credit balance in the allowance account is an estimate amount in an adjusting entry that debits the income statement account bad debts expense and credits allowance for doubtful accounts. In the allowance for doubtful accounts method, bad debts expense is estimated and recognized in the period in which the relevant revenue is recognized. Use an allowance for doubtful accounts entry when you extend credit to customers. So, you can calculate the provision for.

Unlike the direct write off method, the balance sheet here provides an accurate record of the expenses. Allowance for doubtful accounts, bad debt expense accountanting steps when customers who owe do not pay. The expense is booked to the general ledger once all credit and collection efforts on a client's account are utilized and exhausted. Allowance for doubtful accounts primarily means creating an allowance for the estimated part of the accounts that may be uncollectible and may become bad debt and is shown as a contra asset account that reduces the gross receivables on the balance sheet to reflect the net amount that is expected to. An allowance for selected doubtful debts is recorded.

Writing Off an Account Under the Allowance Method ... from www.accountingcoach.com The bad debt expense for the accounting period is recorded with the following percentage of accounts receivable method journal. (1) general provision for doubtful debts: Unlike the direct write off method, the balance sheet here provides an accurate record of the expenses. What is allowance for doubtful accounts? Accounting for doubtful debts presupposes credit sales, so begin by recording the sale in the general journal. The percentage of sales method and the accounts. Unlike bad debt, doubtful debt isn't officially uncollectible debt. Allowance for doubtful accounts, bad debt expense accountanting steps when customers who owe do not pay.

This method allows us to make an estimate, throughout the year, while our revenue is being recognized and our a/r balances are accumulating.

Allowance for doubtful accounts primarily means creating an allowance for the estimated part of the accounts that may be uncollectible and may become bad debt and is shown as a contra asset account that reduces the gross receivables on the balance sheet to reflect the net amount that is expected to. Provision / allowance for doubtful accounts (afda) method: Allowance for doubtful debts or also known as provision for doubtful debts are liabilities that we allocate for any possible non payment by the debtors. So it is kept on the liabilities side of the balance sheet. Using the allowance for doubtful accounts is particularly important to maintain financial statement accuracy, which should be important to any. Using an allowance for doubtful accounts formula lets you anticipate future bad debt expense and prepare for its effects on the financial health of to calculate the amount of the doubtful accounts journal entry, add the current positive or negative account balance to your allowance estimate so the. The expense is booked to the general ledger once all credit and collection efforts on a client's account are utilized and exhausted. An allowance for doubtful accounts is considered a contra asset, because it reduces the amount of an asset, in this case the accounts receivable. The allowance is established in the same accounting period as the original sale, with an offset to bad debt expense. (1) general provision for doubtful debts: The percentage of sales method and the accounts. How business firms face the reality that not all of their customers are going to pay what they owe. The bad debt expense account is the only account that impacts your income statement by increasing expenses.

The allowance for doubtful debts is created by forming a credit balance which is netted off against the total receivables appearing in the balance sheet. The bad debt expense account is the only account that impacts your income statement by increasing expenses. The statement contains the following information The provision for doubtful debt shows the total allowance for accounts receivable that can be written off, while the adjustment account records any changes company a decides to create a provision for doubtful debts that will be 2% of the total receivables balance. Using the allowance for doubtful accounts is particularly important to maintain financial statement accuracy, which should be important to any.

Bad and doubtful debts L3S2 - KashifAdeel.com from kashifadeel.com The allowance is established in the same accounting period as the original sale, with an offset to bad debt expense. Allowance for doubtful accounts, bad debt expense accountanting steps when customers who owe do not pay. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company's balance sheet, and is listed as a deduction immediately below the accounts receivable line item. The bad debt expense for the accounting period is recorded with the following percentage of accounts receivable method journal. This is usually expressed as a % of closing trade receivables and is usually estimated on the basis of past trend and future expectation about the. So, you can calculate the provision for. The allowance for doubtful debts is created by forming a credit balance which is deducted from the total receivables balance in the statement of financial position. Unlike the direct write off method, the balance sheet here provides an accurate record of the expenses.

Allowance for doubtful debts or also known as provision for doubtful debts are liabilities that we allocate for any possible non payment by the debtors.

The percentage of sales method and the accounts. The allowance for doubtful debts contains primarily individually impaired trade receivables from debtors placed under liquidation or companies which are in plant and equipment (a decrease of usd 5,873), change in allowance for doubtful debts (a decrease of usd 1,337 thousand), tax fines and. Although sometimes, it may be an exact figure, as we'll see below. Be sure not to record the bad debt. This is usually expressed as a % of closing trade receivables and is usually estimated on the basis of past trend and future expectation about the. This works in the same way as accumulated depreciation is deducted from the fixed asset cost account. Bad debt expense is the loss from doing business with customers who are later unable to pay for the services or goods they received. The allowance is established in the same accounting period as the original sale, with an offset to bad debt expense. The expense is booked to the general ledger once all credit and collection efforts on a client's account are utilized and exhausted. The term general is used when there is no clear evidence that which trade receivable will not clear his debt. Unlike bad debt, doubtful debt isn't officially uncollectible debt. The allowance for doubtful accounts is a contra account that records the percentage of receivables expected to be uncollectible. The bad debt expense for the accounting period is recorded with the following percentage of accounts receivable method journal.

Belum ada Komentar untuk "Allowance For Doubtful Debts / Chapter 8 Reporting and Interpreting Receivables, Bad Debt ... - It is an unavoidable cost of doing."

Belum ada Komentar untuk "Allowance For Doubtful Debts / Chapter 8 Reporting and Interpreting Receivables, Bad Debt ... - It is an unavoidable cost of doing."

Posting Komentar